Changes to superannuation contribution caps and limits

By Prime Advisory, 29 April 2021

Table of Contents

The Government has announced some very important changes to super and how Australians can save for their retirement. Changes to superannuation contribution caps and limits

In our February 2021 Newsletter, we discussed the general transfer balance cap (TBC) – the limit on the amount you can transfer into the tax-free retirement phase in super – is increasing from $1.6 million to $1.7 million on July 1.

From July 2021, concessional contributions will increase from the current limit of $25,000 p.a. to $27,500 p.a. and non-concessional contributions will increase from $100,000 p.a. to $110,000 p.a.

Kindly note: The advice contained in this article is of a general nature only. It has been prepared without considering your individual goals and objectives, or financial situation. Before making any decision about your super, please consider your personal circumstances and consult with your senior advisor at PrimeAdvisory.

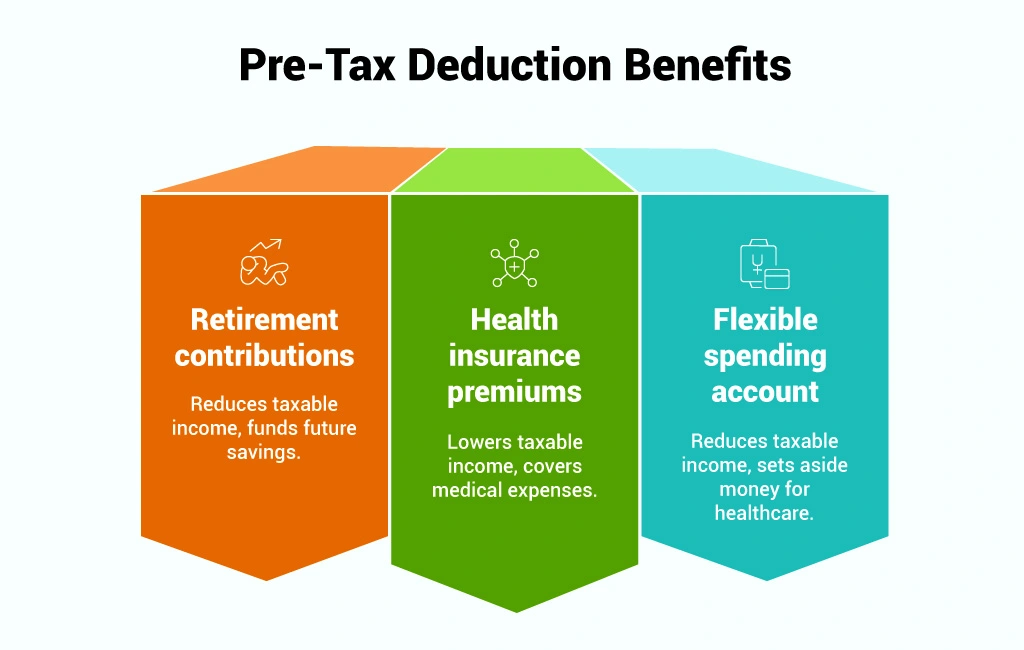

Concessional (pre-tax) Contributions

From July 1, 2021 the annual concessional contributions cap is being indexed from $25,000 to $27,500.

These are pre-tax super contributions and include an employer’s compulsory award, Superannuation Guarantee (SG) and additional voluntary contributions – including salary-sacrifice – and personal contributions you may make for which you claim a tax deduction.

For people making voluntary pre-tax contributions, the increase in the cap for the 2021-22 financial year onwards will likely mean a bigger deduction and tax saving.

However, please be aware if you are a wage-earner and your employer pays the super fund’s administration fees and/or insurance premiums on your behalf, these amounts also count towards your cap.

The SG rate is legislated to increase from 9.5 per cent to 10 per cent from July 1, but there is considerable lobbying in the wake of the COVID-19 crisis to delay this increase once again. So, if you are wage-earning, the opportunity to make increased voluntary concessional contributions from July 1 will be partly absorbed by the increase in your employer’s SG contributions, provided the government does not postpone it.

If you want to use the catch-up rule this financial year – that is, you intend making additional contributions by utilising unused cap amounts from previous years – then you can only do it where you did not utilise the full $25,000 cap in 2018-19 and/or 2019-20, and your total superannuation balance – the total of everything you have in the super system – on June 30, 2020, was less than $500,000. The opportunity arises from unused cap amounts from previous years and until July 1 this year, the concessional contribution cap is $25,000 a year. The higher $27,500 cap does not come into play until the 2021-22 financial year.

If you wish to use the “contribution reserving strategy” in June this year to claim a larger tax deduction in 2020-21, then be mindful that the maximum deduction may be $52,500 (up from $50,000) with the second contribution now being up to $27,500 because it is being tested against the cap in 2021-22 – and do not forget to allocate this contribution by July 28.

Non-Concessional (after-tax) Contributions

From July 1, personal after-tax contributions are on the rise too.

The non-concessional contributions annual cap – currently $100,000 – is four times the concessional contribution cap. Accordingly, with the concessional cap increasing to $27,500, the non-concessional cap will increase to $110,000.

Your total superannuation balance (TSB) determines your eligibility to make non-concessional contributions and relates to the general TBC.

With the TBC increasing to $1.7 million from July 1, it means that if your TSB on June 30, 2021 is less than $1.7 million you may be able to make non-concessional contributions of at least $110,000 next financial year (i.e., in 2021-22). Without indexation of the TBC, you would have been unable to contribute if you had between $1.6 million and $1.7 million in super.

Your TSB also determines your entitlement to use the non-concessional bring-forward rule to get more into super. There are some complicated calculations to understand your bring forward rule, particularly if your individual balance is more than $1.48m as at 30 June 2021.

Salary-Sacrifice and Personal Contribution Rules

Your eligibility to contribute to super is reliant on your age. Anyone under 67 may contribute, but if you are 67-74, you must meet the work test (40 hours of gainful employment in 30 days) or work test exemption to contribute.

The work superannuation test exemption may be used to contribute to super – provided you have not used it before – where you had no more than $300,000 in super at the previous June 30 and you met the work test in the last financial year.

You cannot contribute after 28 days after the end of the month in which you turn 75. Only employer-mandated award and SG contributions can be made.

While the age to make super contributions without meeting the work test or work test exemption has been extended to people aged 65 and 66, the extension of the non-concessional contribution bring-forward rule for people in this age group has not – yet.

Note that the age restriction, work test and TSB test do not apply to downsizer contributions.

The long-awaited indexation of the contribution caps and the transfer balance cap superannuation is a much-needed relief for the superannuation system. It was wished that it would have occurred last year – but it did not. So, it is wonderful news it is finally happening this year.