Payday Super is Coming: What Employers Need to Know

By Prime Advisory, 23 February 2026

From 1 July 2026, quarterly super payments are out. Payday Super is in.

If you’re an employer, this changes your payroll process, cash flow, and compliance obligations. If you’re an employee, your super arrives faster – every payday instead of quarterly.

Here’s what employers need to know.

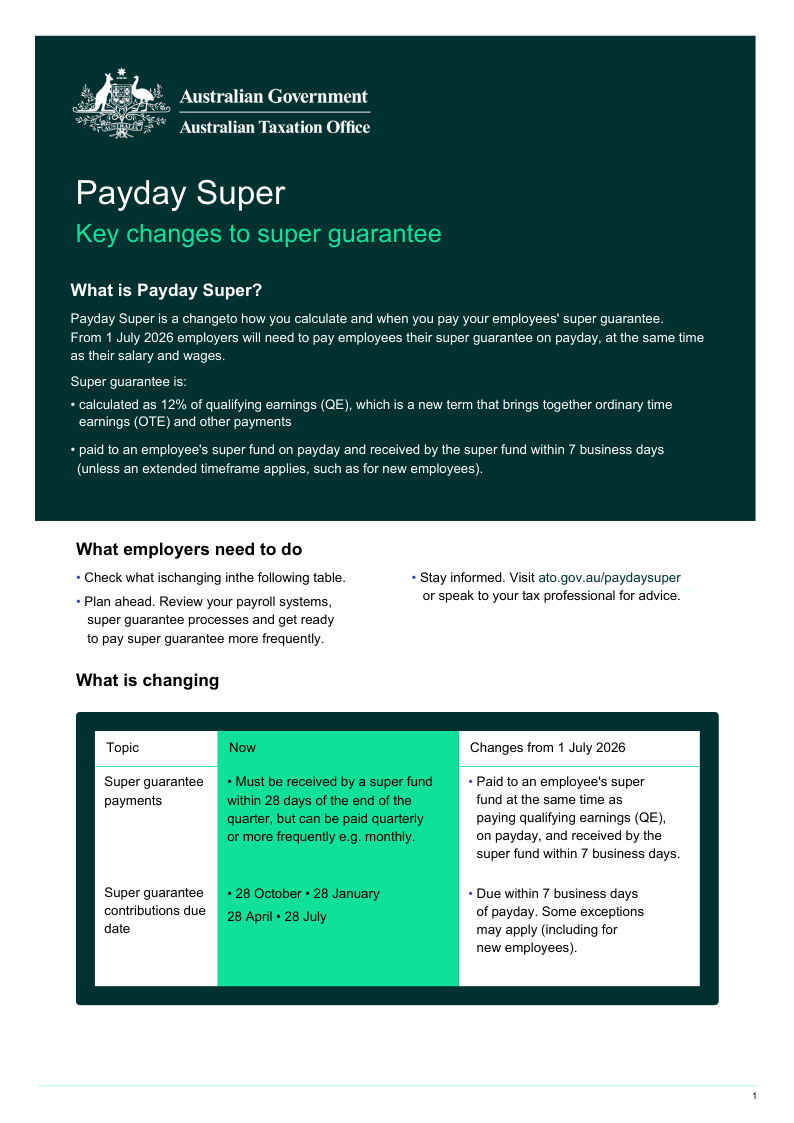

What is Payday Super?

From 1 July 2026, you’ll pay your employees’ super guarantee on payday, at the same time as their salary and wages. Super contributions must be received by the super fund within 7 business days of payday.

This is the biggest change to employer super obligations in over a decade. It means tighter deadlines, more frequent payments, and stricter penalties for non-compliance.

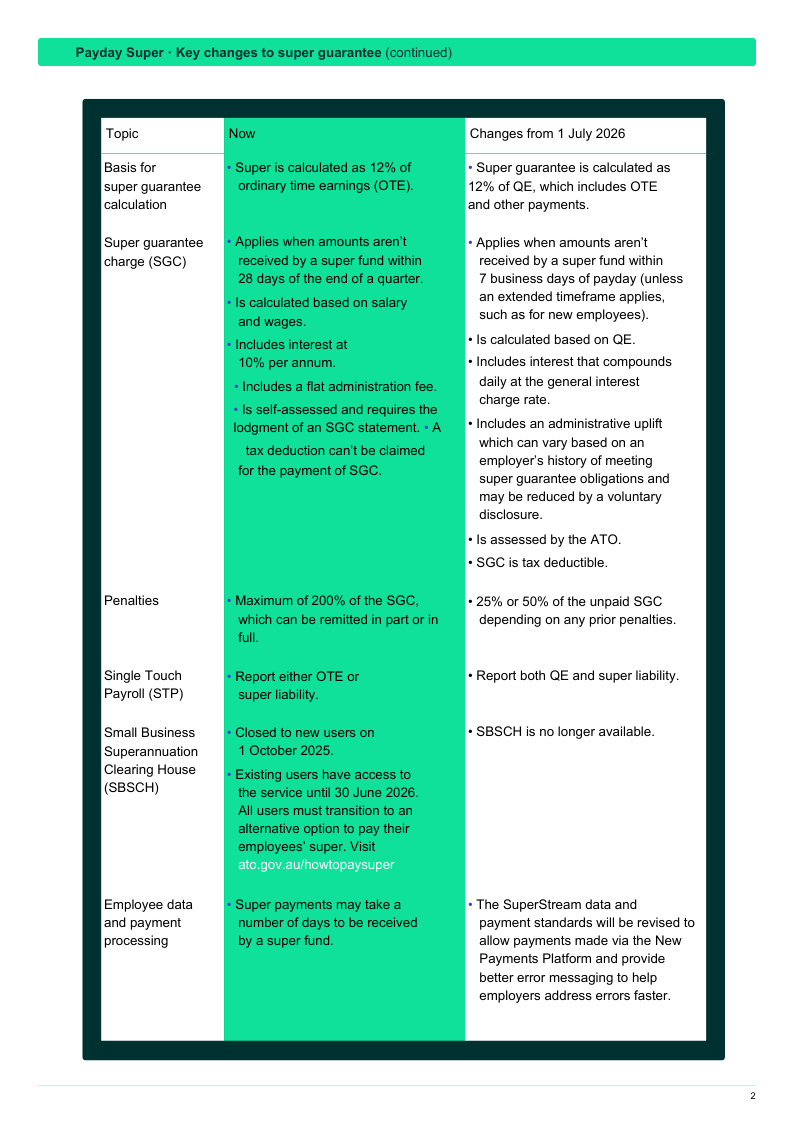

What’s Changing: Old vs New

Here’s what you need to know about how Payday Super differs from the current system.

The shift from OTE to Qualifying Earnings could mean you’re calculating super on a broader base of payments. QE includes everything in OTE (regular wages, salaries, commissions) plus additional payments, such as certain allowances, bonuses, and salary sacrifice amounts, that weren’t previously captured. The exact impact depends on your pay structure.

That’s something to review with your advisors now, not in June 2026. The ATO has published detailed guidance on QE at ato.gov.au/QE

The Small Business Super Clearing House is Closing

If you currently use the ATO’s Small Business Superannuation Clearing House (SBSCH), here’s critical information: it closes permanently on 30 June 2026.

You won’t be able to log in after 11:59 pm AEST on that date. Your final payment through the SBSCH should be for the January to March 2026 quarter, due 28 April 2026.

Before 30 June, you need to:

- Download all employee payment transaction records

- Download all employee details (name, super fund, member numbers)

- Transition to an alternative payment method

The April to June quarter payment (due 28 July 2026) cannot be made through the SBSCH. You’ll need your new system ready to go.

Three Critical Preparation Steps

1. Review Your Payroll System

Your payroll software needs to calculate super on Qualifying Earnings (not just OTE – Ordinary Time Earnings ), submit payments electronically via SuperStream, and handle weekly or fortnightly payment cycles without manual work.

If you’re using spreadsheets or older software, you’ll struggle with Payday Super. Modern systems like Xero are built for this kind of compliance and handle everything automatically.

2. Plan Your Cash Flow

Paying super on every payday instead of quarterly changes your cash flow cycle. You need to factor super into each pay run, not just four times a year.

Model what this looks like for your business. Make sure you can comfortably pay super with each pay cycle from July onwards.

3. If You Use the SBSCH, Transition Now

The Small Business Superannuation Clearing House closes permanently on 30 June 2026. Your final payment through it should be in April for the January to March quarter.

You need an alternative in place before then. Most businesses are transitioning to integrated payroll software like Xero.

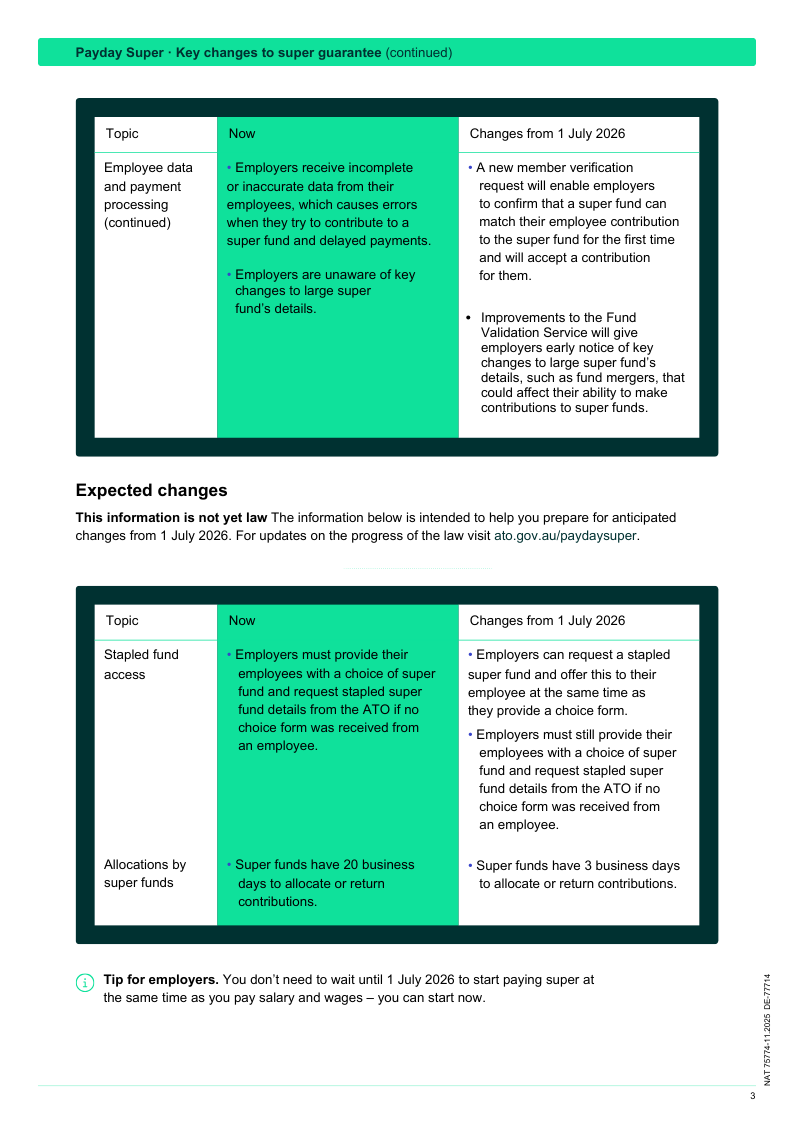

SuperStream Improvements Coming Too

At the same time Payday Super launches, the ATO is upgrading SuperStream to version 3. Key improvements include:

- Member verification requests to catch errors before payments

- Better error messaging for faster problem resolution

- Faster payments through the New Payments Platform (same-day delivery possible)

- Early warnings about super fund changes, like mergers

Modern payroll software, such as Xero, will automatically integrate these improvements.

Who Can Help

For operational questions about how Payday Super affects your day-to-day payroll, speak with your bookkeeper. They can help with process questions, software settings, and routine compliance.

For strategic planning around your transition, we can help:

If you need to plan how Payday Super affects your cash flow and business operations, we can model the impact and help you prepare.

If your payroll system isn’t ready and you’re considering a software transition, we’re Xero partners and can manage your complete conversion – from assessment through to implementation and training.

If you’re using the SBSCH and need to transition by June 2026, we can review your options and recommend the right solution for your business.

Payday Super requires the right systems. If you’re unsure whether yours are up to the task, now’s the time for a software and process review.

Book a consultation: (02) 9415 1511 | [email protected]

We make more possible with your money, including making compliance simpler through smarter systems.

FAQs

1. What exactly is “Qualifying Earnings (QE)”?

QE is the new definition of employee earnings used to calculate the 12% “Superannuation Guarantee (SG)”. Employee earnings as defined under the “Ordinary Times Earnings (OTE)” rule will no longer apply. QE is an expanded concept of OTE and includes some types of employee payments not previously included in OTE.

2. What is the “7 business day” rule—does it mean I can pay super up to 7 days after payday?

Not quite. The core compliance test is that the contribution must be received by the super fund within the required window (i.e. within 7 business days of payday). So even if you “send” the payment earlier, processing times (e.g. banking + clearing house + fund acceptance) becomes the risk point, because the clock stops when the fund receives the contribution.

3. Under Payday Super, when is super actually considered “paid”, and has that changed?

For most employers, this hasn’t changed in principle: super is generally only considered “paid” when the superannuation contribution is received by the employee’s super fund, not when received by a commercial clearing house.

4. What changes in “Single Touch Payroll (STP)” reporting once Payday Super starts?

From 1 July 2026, the ATO will require that employers report both the QE and the superannuation liability via STP. STP reporting will become a tighter reconciliation loop between what the employer has paid (the “QE”) and the amount of superannuation owed to the employees’ fund.

5. Are there specific transition/operational impacts small employers should plan for (beyond “more frequent payments”)

Yes—two big ones commonly missed:

- Payroll systems and pay events need to handle more frequent, shorter-cycle super payments and the associated data quality steps (member verification, fund details accuracy, handling contribution rejections/refunds) because a rejected payment can quickly become “late.”

- The “Small Business Superannuation Clearing House (SBSCH)” is being retired from 1 July 2026 (and is already closed to new users earlier), meaning small employers who relied on it need an alternative superannuation provider.