The 2026 Federal Budget: The Three Changes That Reshape Property, CGT and Family Trusts

By Prime Advisory, 13 May 2026

On Tuesday, 12 May 2026, Treasurer Jim Chalmers handed down the 2026-27 Federal Budget. Some Budgets are boring. This one is not.

Most of the headline announcements are minor. A $1,000 instant work-related deduction. A $250 Working Australians Tax Offset. A small lift to the Medicare levy low-income thresholds. None of it changes the planning equation for the families we work with.

Three other measures do.

The 50% capital gains tax discount that has shaped Australian investment behaviour since 1999 is being replaced. The way family trusts are taxed is changing in a way that materially alters one of the most common structures used by professional families and business owners in Australia. And negative gearing on established residential investment property is being wound back.

These are structural changes, not incremental tweaks. None of them is law yet. All of them are now on the table, and the direction of travel is clear.

Here is our full take on what was announced, what it means in practice, and where the planning windows sit.

1. The 50% CGT discount is being replaced

This is the change with the broadest reach. It does not just affect property investors. It affects everyone who holds appreciating assets in their own name, through a trust, or through a partnership.

The 50% CGT discount has been a feature of the Australian tax system since 1999. Hold an asset for more than 12 months, and the gain is effectively taxed at half your marginal rate. It has shaped how families invest, how they structure asset ownership, and when they choose to sell.

From 1 July 2027, that discount is being replaced by two mechanisms working together:

1. Cost-based indexation, similar to the system that ran from 1985 to 1999. The cost base of an asset held more than 12 months is indexed for inflation using the Consumer Price Index.

2. A 30% minimum tax on net capital gains that accrue from 1 July 2027 onwards.

The transitional rules are important. Gains that accrued before 1 July 2027 retain the existing treatment, including the 50% discount and the pre-CGT exemption for assets acquired before 20 September 1985. To make this work, taxpayers will need to determine the value of their existing assets at 1 July 2027. That valuation becomes the cost base going forward.

This applies to all asset classes, including property and shares, held by individuals, trusts, and partnerships. Recipients of means-tested income support payments such as the Age Pension or JobSeeker get an exemption from the 30% minimum tax. New residential property investors can choose either method (the existing discount or the new indexation plus minimum tax) at the time of sale.

The practical implication is that planning around capital gains becomes considerably more complex. The maths on when to sell, which entity to hold an asset in, and how to manage realisation timing all change. A 1 July 2027 valuation exercise becomes a meaningful piece of work for anyone holding material appreciating assets.

2. Family trust distributions face a 30% minimum tax

For the professional families we work with, the overhaul of trust taxation represents the most profound structural shift in this Budget.

Beginning 1 July 2028, discretionary trust income will be subject to a 30% minimum tax at the trustee level. While individuals and most non-corporate beneficiaries will benefit from a non-refundable tax credit, corporate beneficiaries are specifically excluded from this mechanism.

While the first impacted filings won’t occur until the 2028-29 tax year, typically lodged in late 2029, the planning window is narrower than it appears. Evaluating whether to maintain current structures with adjusted distribution strategies, or to pursue a total restructure, is a significant undertaking, particularly for trusts holding illiquid or complex assets.

This effectively dismantles the “bucket company” strategy, a cornerstone of Australian tax planning for decades. By removing the credit for corporate beneficiaries, the government has materially increased the effective tax rate for income flowing through a trust to a company, changing the math for small business owners and professional families alike.

A selection of entities remains outside these new rules. Fixed trusts, super funds, charitable organisations, and deceased estates are unaffected. Furthermore, primary production income and specific distributions from testamentary trusts established before the Budget announcement are also exempt from the 30% minimum tax requirement.

To facilitate the transition, the Government will provide three years of rollover relief starting 1 July 2027. This is intended to mitigate the federal income tax burden of moving into a company or fixed trust structure, though state-based costs like stamp duty remain a critical variable that must be assessed on an individual basis.

Our existing family trust strategy and trust review process are still relevant for the next 2-3 years while these proposals are finalised, so there’s no need for a sudden rethink. We’re watching this closely. Once the changes are confirmed, we’ll share exactly what we think the best path forward is.

3. Negative gearing is being restricted to new builds

The change most likely to affect our clients’ day-to-day investment decisions is the restriction on negative gearing.

From 1 July 2027, losses on established residential investment properties acquired from 7:30 pm AEST on 12 May 2026 will only be deductible against rental income or capital gains from residential property. They will no longer be available to offset salary, business income, or other unrelated income. Any excess loss carries forward to be used against future residential property income.

Properties acquired before last night are fully grandfathered. Existing investors keep the current treatment indefinitely. New builds remain fully deductible against any income, as the policy intent is to channel new investment into properties that genuinely add to housing supply.

The fine print matters. “New builds” means residential property that genuinely adds to supply, such as a dwelling built on vacant land or a project that demolishes one dwelling and replaces it with several. Knock-down rebuilds or substantial renovations that do not increase the dwelling count are not treated as new builds. Commercial property, shares, managed investment trusts, and superannuation funds are all unaffected.

For investors who are actively in the market right now, the question has shifted from when to buy to what to buy. The grandfathering window for established residential property closed at 7:30 pm AEST on Tuesday. Any established property bought from now on falls under the new ring-fencing rules from 1 July 2027.

If you have a purchase planned in the next 6 to 12 months, the live decision is whether to commit to an established property and accept the post-2027 treatment, or to pivot to a new build and retain full deductibility against any income.

For investors who are already holding established residential property, nothing changes today. The grandfathering is genuine.

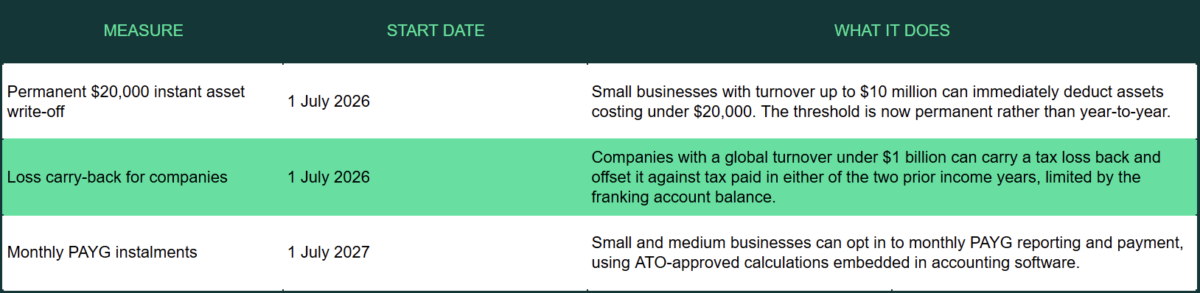

What was good news in the Budget?

The Budget was not all friction. There were three measures that genuinely help business owners and small companies.

There were also some changes to the FBT exemption on electric vehicles (gradually scaled back from 1 April 2027), reforms to the R&D Tax Incentive (from 1 July 2028), and the loss refundability scheme for early-stage start-ups (from 1 July 2028). For most of our clients, these are useful to know but not structurally significant.

A necessary reminder

Each of the measures discussed above is an announcement at this point. None of it is law yet. Legislation has not been drafted, let alone passed. The detail will move as the process unfolds. Some measures may not be implemented at all, and others may look quite different by the time they take effect.

That is not a reason to wait and see. The proposed start dates for the major measures are tight (1 July 2027 for negative gearing and CGT, 1 July 2028 for trusts), and the planning required to take advantage of the grandfathering, the rollover relief, and the transitional rules is substantial.

It is a reason to plan deliberately rather than react.

The 18-month planning window

If you hold investment property, run income through a family trust, or are sitting on assets with material unrealised gains, the next 18 months matter.

The 1 July 2027 effective date for the major property and CGT changes creates a defined window for valuing assets, considering disposals, and assessing structures. The 1 July 2027 opening of the trust restructure rollover relief, running for three years to 30 June 2030, defines the window for trust decisions. The grandfathering on negative gearing is permanent for properties acquired before 7:30 pm AEST on 12 May 2026, which sets the timing question for anyone considering an investment purchase right now.

None of these decisions are urgent in the next week. All of them benefit from being made with the full structure in view, rather than in response to a single announcement.

What to do now

We have put together a full 2026 PrimeAdvisory Budget Summary covering each measure in detail, with the timing, eligibility, and planning implications clearly laid out.

Download the 2026 PrimeAdvisory Budget Summary

If you would like to discuss how any of the changes apply to your specific situation, your investment property, your trust, your business structure, or your overall plan, the best step is a conversation. Reach out to your usual PrimeAdvisory contact, or book a time, and we will work through it together.