Transferring Property to a Family Member in Australia: 2026 Tax & Legal Guide

By Prime Advisory, 21 July 2026

The question every family eventually asks

Most families we work with eventually run into the same question. How do I move this property to my kids (or my spouse) without a tax shock?

The answer is that transferring property to a family member can happen three different ways, and the tax treatment of each is very different. A draft ATO determination released in 2026 has just narrowed one of those paths, so getting this right matters more this year than it did last.

This guide walks through the options, what each costs in tax and duty, and how we think about the decision when an Australian family asks us which way to go.

Three ways property changes hands in a family

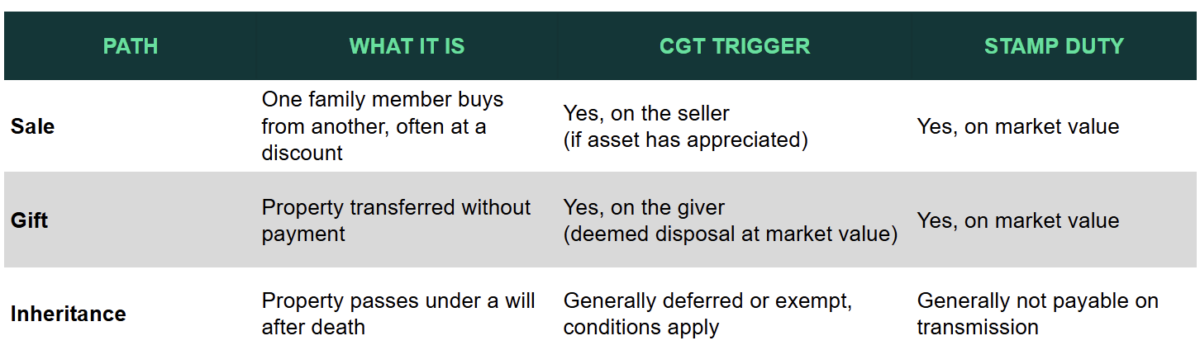

There are three legal mechanisms. Most families assume one of them is “tax free.” It usually isn’t.

No path is tax-free in every situation. Which one fits depends on the property, the family member, and the broader structure.

Selling property to a family member

This is the path families instinctively reach for. The thinking is usually: I’ll sell it to my daughter for a discount, she’ll get a great deal, problem solved. It rarely works that way.

Stamp duty is assessed on market value, not the sale price. Sell to your daughter for $1, and the applicable State Revenue Office will substitute their own valuation. There is no family discount.

Capital gains tax applies to the seller. If the property has appreciated, the gain is assessed in the year of sale. The 50% discount may apply if you’ve held it more than 12 months, though CGT settings are under review, with changes flagged from 1 July 2027. The main residence exemption may apply if it’s been your home. For an investment property worth $1.8M with a $700,000 gain, the bill at the top marginal rate, after the discount, can land north of $160,000.

A family sale still works when the buyer can genuinely fund the purchase and the seller actually wants the cash. Often, the seller uses the proceeds to top up their super or pay down any debt. In that case, the sale is a real transaction, and the tax is the cost of doing business cleanly.

Gifting property to a family member

A gift sounds simple. No money changes hands, so no tax. The ATO sees it differently.

When you gift property, the ATO deems you to have sold it at market value on the day of transfer. Even though you’ve received nothing, you owe CGT on the gain since you bought it. For a holiday house bought twenty years ago and now worth $1.5M, with a $1M gain, the bill can be substantial. Stamp duty is also assessed on market value, same as a sale.

The point most families miss is the second-order effect. Once the property is in your child’s name, you’ve also handed over the rates, the land tax, and any future exposure to a divorce settlement or creditor claim against the new owner. A lot of families gift assuming the property is “looked after,” only to realise they’ve also transferred a financial burden onto someone who may not be ready for it.

Transferring property to a spouse

Spouse transfers sit in their own bucket. NSW, Victoria, Queensland and the ACT offer concessions or exemptions from stamp duty for transfers of the principal place of residence between spouses. The CGT main residence exemption flows through if the property has genuinely been the couple’s main residence. Investment property transfers between spouses do not get the same treatment.

Inheriting the family home (and the 2026 ATO update)

The third path is inheritance. For most Australian families, the family home is the largest single asset that will ever change hands, and the main residence exemption can deliver the biggest single tax saving in a family’s lifetime, if the will is set up correctly.

If a beneficiary inherits the deceased’s main residence and sells within two years of the date of death, the sale is generally exempt from CGT. The exemption also flows through if the property is occupied as the main residence of the surviving spouse, a beneficiary disposing of it, or a person who had a right to occupy the dwelling under the deceased’s will. Our existing guide on capital gains tax on inherited property walks through the details.

That last condition, “a right to occupy under the deceased’s will,” is where things have just changed.

What TD 2026/D1 actually says

In early 2026 the ATO released Draft Taxation Determination TD 2026/D1. The Commissioner’s view is now that the right to occupy must be explicitly granted in the will to a named individual. Broad executor discretion, or testamentary trust arrangements where the trustee can grant occupancy, are no longer enough on their own.

If the will simply gives the executor or trustee discretion to “permit any beneficiary to occupy the dwelling,” the ATO’s draft view is that the main residence exemption may not flow through. The condition has not been met because no specific person was granted the right.

The practical consequence is straightforward. A $2 million home with a $1.5 million unrealised gain could expose the beneficiaries to $300,000 to $600,000 in CGT, depending on the discount and marginal rates. Same family, same house, but a will written in 2018 now produces a very different outcome under the ATO’s draft view.

The fix is simple. A current, well-drafted will, ideally reviewed alongside any testamentary trust. If your estate plan relies on a Testamentary Trust to hold the family home, our trust health and hygiene check is the place to start. The broader estate planning guide covers the rest.

Transfer now, or wait?

This is the strategic question, and it’s where families get the most value from sitting down with an adviser.

The reality is that there’s no universal answer. Transferring during your lifetime tends to make sense when the giver has more than they need, the recipient genuinely needs the support, and the property has not appreciated significantly, so the CGT bill on disposal is small. Helping an adult child onto the property ladder is the most common case we see.

Waiting for inheritance tends to win when the property is the family home, the main residence exemption is available, and the parents need the asset (or the borrowing capacity it represents) for retirement. Provided the will is current under TD 2026/D1, the inheritance path remains the cleanest tax outcome for most family homes.

In practice, most families end up with a hybrid: keep the family home until inheritance, move investment properties through a trust restructure during life, and use a testamentary trust in the will for whatever’s left.

The clients who get this right treat property transfer as part of a broader wealth plan, not a one-off transaction. That’s the difference between a clean handover and a tax bill nobody saw coming.

How PrimeAdvisory works with families on this

“Prime is always pulling us up on exposures before they ever become a risk.”

Greg Baird, SBA Architects

Most families come to us with one specific transfer in mind and walk away with a plan that covers every transfer they’ll need to make over the next 30 years. Property rarely sits in isolation. It’s part of the broader question of how the family group passes wealth from one generation to the next.

If this is something you’re thinking through, a conversation is the cheapest part of getting it right.

Frequently asked questions

Do I pay capital gains tax when I gift property to my child in Australia?

In most cases, yes. The ATO treats the gift as a deemed sale at market value. The 50% discount may apply if you’ve held it more than 12 months, though CGT settings are under review, with changes flagged from 1 July 2027. The main residence exemption may apply if it’s been your home. For an investment property or holiday house, expect a tax bill.

Is stamp duty payable when property is transferred between family members?

In nearly every case, yes. Stamp duty is assessed on market value, regardless of what the family agrees to pay. Some states offer narrow concessions for spouse transfers of the principal place of residence. There is no broad family exemption for transfers to children, grandchildren, or siblings.

What is the 2-year rule for inherited property?

If a beneficiary inherits the deceased’s main residence and sells within two years of the date of death, the sale is generally exempt from CGT. The Commissioner has discretion to extend in specific circumstances, such as probate delays or contested estates, but two years is the working rule.

Can a testamentary trust still hold the family home tax-free?

Following TD 2026/D1, only if the will explicitly grants a named individual the right to occupy the dwelling. A testamentary trust with broad trustee discretion is no longer enough on its own to preserve the main residence exemption, in the ATO’s draft view. Wills relying on this structure should be reviewed.

Take the next step

If transferring property to a family member is on your mind, or you’ve put it off because the tax position looked complicated, book a strategy session with PrimeAdvisory and we’ll map the right path for your situation.